Why Tax Residency Matters

When you launch a business in Singapore, it’s natural to get caught up in the numbers. Founders may focus on tax exemptions and how to maximise the Start‑Up Tax Exemption (SUTE) scheme to protect their first chunks of revenue. However, many skip the step to check if they meet Singapore’s tax residency test.

Singapore does not determine corporate tax residency by where a company is registered. Incorporation may give you a local address and a UEN, but it does not automatically make you a Singapore tax resident in the eyes of the Inland Revenue Authority of Singapore (IRAS). The coveted residency status relies on a different, much tougher test. It all comes down to a concept known as “Control and Management.” Beyond SUTE, Singapore tax residency is also the gateway to Singapore’s network of over 100 double tax agreements.

For a solo founder who runs the business entirely in Singapore, this is rather straightforward. But for cross‑border ventures with overseas co‑founders, distributed teams, or boards that meet remotely, proving residency requires planning. In this article, we’ll break down exactly how tax residency is established and how to apply for the Certificate of Residence (COR) to prove your status.

What is the Certificate of Residence (COR)?

The Certificate of Residence (COR) is an official document issued by IRAS that proves Singapore tax residency to a foreign tax authority for a specified period. Think of the COR as your company’s tax passport. A passport doesn’t make you a citizen, but it proves you are one. The COR works the same way, it helps to certify Singapore tax residency.

Foreign tax authorities often request the COR when a Singapore company seeks to claim benefits under a double tax treaty. This certificate is the proof that allows businesses to access reduced withholding tax rates, treaty relief, and recognition of Singapore residency in cross‑border transactions.

IRAS does not simply hand out a blanket certificate that covers your company indefinitely. To apply, you must specify two things: (1) the treaty partner country you are dealing with, and (2) the Year of Assessment (the relevant tax year) you need certification for. Each COR is tied to a specific country and a specific Year of Assessment, which means you will need separate certificates if you are claiming benefits across multiple jurisdictions or tax years. Everything is handled digitally through the myTax Portal. When IRAS approves your application, they issue an official electronic PDF letter.

The Difference Between Incorporation and Residency

One of the most common mistakes founders make when expanding into Singapore is assuming that incorporation automatically leads to tax residency. But that is not the case. Incorporation ≠ tax residency.

Incorporation determines where a company is legally established. Tax residency is about where the company is directed and controlled. It is assessed by IRAS on an ongoing basis and determines which jurisdiction has the primary right to tax the company’s profits. Put simply, where your company is registered matters, but where its key decisions are made matters more.

Let’s consider a Japanese company that establishes a subsidiary in Singapore. Its shareholders remain Japanese corporate entities, but the company appoints a Singapore-based Managing Director, maintains a majority of Singapore-resident directors, and conducts its quarterly board meetings in Singapore. Although foreign-owned, the company’s strategic decisions are made locally. From IRAS’s perspective, this is a strong indicator that control and management are exercised in Singapore, supporting its status as a Singapore tax resident.

This distinction is more than a technicality. Tax residency is the foundation upon which a COR is issued. The certificate does not create residency. Before a company can benefit from Singapore’s tax treaty network, it must first demonstrate that it genuinely belongs here from a tax perspective.

When Management Matters More Than Geography

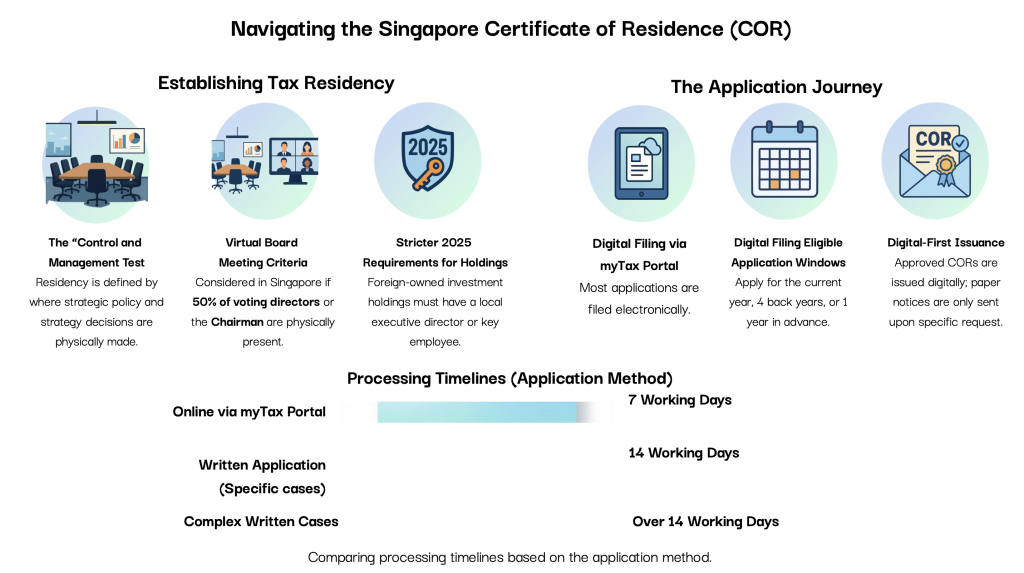

To determine corporate tax residency, IRAS applies the “Control and Management” test. This isn’t about where your employees are based or where day‑to‑day operations take place. It’s about the highest level of decision‑making, where strategy is set, policies are approved, and the board physically meets to steer the company’s direction.

IRAS is looking at substance over form. It is less concerned with formalities and more interested in whether there is a consistent, demonstrable pattern of governance in Singapore. A company may be incorporated locally and hold occasional board meetings in Singapore, but if key decisions, such as approving budgets or negotiating contracts, are effectively made elsewhere, then control and management is unlikely to be regarded as Singapore-based.

This distinction has become even more relevant in an era of distributed teams and virtual meetings. While technology makes it easy to convene boards from anywhere in the world, it also means physical presence alone is no longer sufficient. Companies must be able to show that Singapore is the centre of strategic decision-making, not just a location used for administrative convenience. Hence, IRAS has established strict criteria to handle this shift:

1. The Virtual Board Meeting Rule:

If your directors are dialing in from different corners of the world, IRAS deems the strategic decisions to be made in Singapore only if at least 50% of the voting directors or the Board Chairman are physically present in Singapore during the meeting.

2. Stricter Substance Requirements for Holdings:

For foreign-owned investment holding companies, simply having a local address no longer cuts it. To secure tax residency, these entities must demonstrate deeper local economic substance, such as having a local executive director or a key employee (e.g., CEO, CFO or COO) based on the ground in Singapore.

This means that a COR application that used to sail through with zero issues could get rejected today if your governance structure has not kept up with these new requirements. Before you head into the myTaxPortal, review your current board and executive setup. It is also worth checking in with a qualified Singapore tax advisor to make sure your application isn’t going to be rejected.

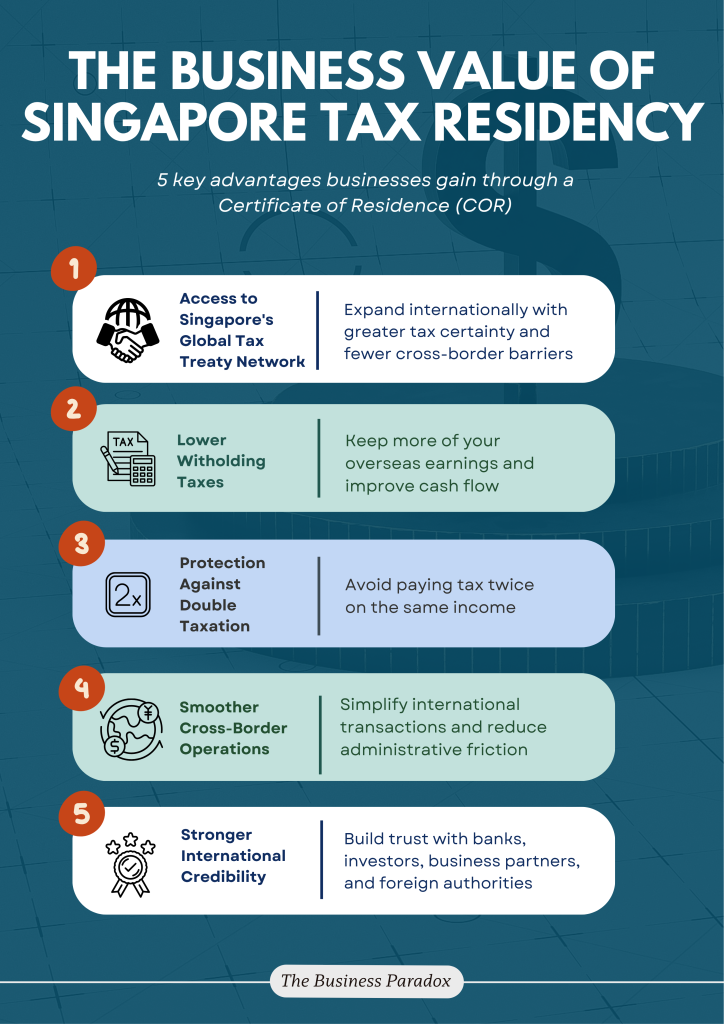

The Advantages of a Singapore Tax Residency

Before looking at the administrative steps involved in applying for a COR, it is important to understand what tax residency actually enables in practice.

At its core, Singapore tax residency determines how a business is recognised in the international tax system. It is the basis on which treaty access, tax treatment, and cross-border positioning are established. As companies expand across borders, they could be earning revenue from multiple markets or licensing intellectual property internationally. Thus, the question of where the business is genuinely based becomes increasingly important. In this context, tax residency is less about formality and more about alignment between how a company operates and how it is recognised externally.

It also plays a quieter but equally important role in how a business is perceived and engaged with. Clear tax residency helps reduce ambiguity when dealing with tax authorities, banks, investors, and commercial partners. Instead of repeatedly explaining structure or operational presence, companies with established residency can move through compliance checks, financial processes, and cross-border transactions with greater ease and predictability.

Taken together, tax residency is what allows the benefits illustrated above. The COR is simply the confirmation of that status and it is the point at which these advantages become recognisable in a cross-border context.

How To Apply for a Certificate of Residence?

The COR application is more straightforward than many expect, because it is filed online through IRAS’s myTax Portal. Each Year of Assessment requires a fresh application, and IRAS has designed the process as a defined sequence where precision at every step matters. That’s because the COR is treaty‑specific, time‑bound, and substance‑driven. The application involve a few key steps:

1. Select Your Timeline: You can apply for the current year, up to four past years, or one advance year (advance applications open from October).

2. Choose the Partner Country: Declare the treaty partner nation where your income originates.

3. Complete the Substance Questionnaire: Foreign-owned entities must prove local management presence, including board meeting venues, executive directors or key employees, and the nature of foreign income claimed.

4. Review and Submit via myTax Portal: Review and finalise your data on the confirmation page and submit the application online.

If you submit a straightforward and prepared case, IRAS typically processes and approves the application within 7 working days. However, if your structure is complex, expect the timeline to stretch to several weeks as IRAS may issue follow-up queries. Once IRAS approves the application, an automated alert will arrive in your inbox within 1 to 3 working days. After this, you can log back into the myTax Portal and download your approved electronic PDF certificate directly.

For more detailed instructions, please refer directly to IRAS’s resources on the COR process. IRAS provides step‑by‑step guidance, eligibility criteria, and the latest compliance requirements to ensure your application is accurate.

Conclusion: Tax Residency as the Cornerstone of Global Business

At the end of the day, how a business is treated in the international tax system comes down to this question: where is it actually being run from? Tax residency is something you demonstrate over time. It reflects where the real decisions are made, where direction is set, and where leadership genuinely sits. In that sense, it says less about paperwork and more about the centre of gravity of your business.

The COR sits on top of that reality. It does not create tax residency and it does not change how a company is governed. What it does is confirm, to tax authorities and counterparties abroad, that your business already meets the standard. It is the formal signal that your structure and your substance are aligned.

That is why how your board operates, where strategic decisions are made, and how those decisions are documented throughout the year all feed into whether that position holds under scrutiny. For founders and leaders running cross-border businesses, don’t wait until residency is questioned from the outside. The earlier you align your governance with Singapore’s requirements, the stronger your position will be when treaty benefits and credibility are on the line.

Stay ahead with exclusive insights! Sign up for our mailing list and never miss an article. Be the first to discover inspiring stories, valuable insights and expert tips – straight to your inbox!