What is the Start-Up Tax Exemption Scheme (SUTE)?

The Startup Tax Exemption Scheme (SUTE) was introduced in Singapore to help new businesses during their early growth years. For qualifying startups, the scheme provides:

- 75% tax exemption on the first S$100,000 of chargeable income

- 50% exemption on the next S$100,000

- For the first three consecutive Years of Assessment (YA)

Importantly, chargeable income is not the same as revenue. It refers to your taxable profit after deducting allowable business expenses and other permitted deductions. For example, if a company generates S$300,000 in revenue but has S$180,000 in allowable expenses, SUTE applies to the remaining S$120,000 of chargeable income.

For growing startups, this can significantly reduce the effective corporate tax rate and free up more capital for hiring, expansion, product development, and growth.

While many founders focus on whether they qualify for SUTE, far fewer think about how to maximise it. The reality is that the way you structure your first financial years, especially your Financial Year-End (FYE) and incorporation timing, can determine how much of your most profitable growth period actually falls within the exemption window.

This article is the first part of a two-part series on how founders can think more strategically about Singapore’s Start-Up Tax Exemption scheme. This first article focuses on timing, specifically, how date of incorporation and FYE choices influence the effectiveness of your exemption window.

The Cost of Poor Timing in Startup Tax Planning

When starting a business, you already have a thousand things on your mind. Naturally, tax planning may be the last thing you want to focus on. Yet, in Singapore, one small administrative decision made during incorporation can quietly affect your cash flow years later. That decision is your FYE.

Most founders choose an FYE without much thought. However, the timing matters more than many realise. Your FYE determines when your first Year of Assessment (YA) begins and that is what starts the clock on SUTE.

The SUTE scheme gives qualifying startups valuable tax relief during their first three consecutive YAs. Even if your company generates little or no profit in the first YA, that year still counts. Once it passes, the unused exemption does not carry forward. This is where many founders unknowingly lose part of the benefit before business even gains momentum.

Timing changes everything.

The SUTE window is something founders can actively shape at the point of incorporation. The moment you decide when to incorporate and what FYE to adopt, you are effectively shaping the boundaries of your exemption period.

After the three SUTE years end, companies typically move to Singapore’s Partial Tax Exemption (PTE) scheme, which still provides tax relief at lower exemption rates. That makes the first three years especially valuable, particularly for startups expecting growth and profitability later in the journey.

Understanding How the 3-Year SUTE Window Actually Works

We first need to understand how Singapore’s tax calendar works. A YA is not the same as a financial year. This distinction matters more than most people realise. In Singapore, a YA refers to the year your company’s income is assessed for tax and the tax itself is based on profits from the previous financial year.

Here’s an example:

- Financial Year End (FYE): December 2025

- Year of Assessment (YA): 2026

- Tax Return is Due By: Nov 2026

That means if your FYE is December 2025, your company will file taxes in YA 2026, with the return typically due in November 2026. The moment you lock in that first FYE, your SUTE countdown clock starts ticking.

Why Financial Year-End Selection Matters

The choice of FYE can directly shape how the SUTE applies to your business. Since Singapore’s tax system ties each YA to your company’s FYE, the date you select determines when your three‑year exemption window begins and ends.

When founders discover that Singapore allows a company’s first financial period to stretch up to 18 months, they often assume that stretching the first financial year automatically buys them more time and more tax savings. But it doesn’t.

In reality, IRAS will only assess a maximum of 12 months of accounts per YA. If your first financial period is longer than 12 months (say, a 15-month period from January 2026 to March 2027), IRAS will legally mandate that those accounts be split across two separate YAs. This may actually burn through SUTE years faster.

How To Align Your Most Profitable Early Years With SUTE

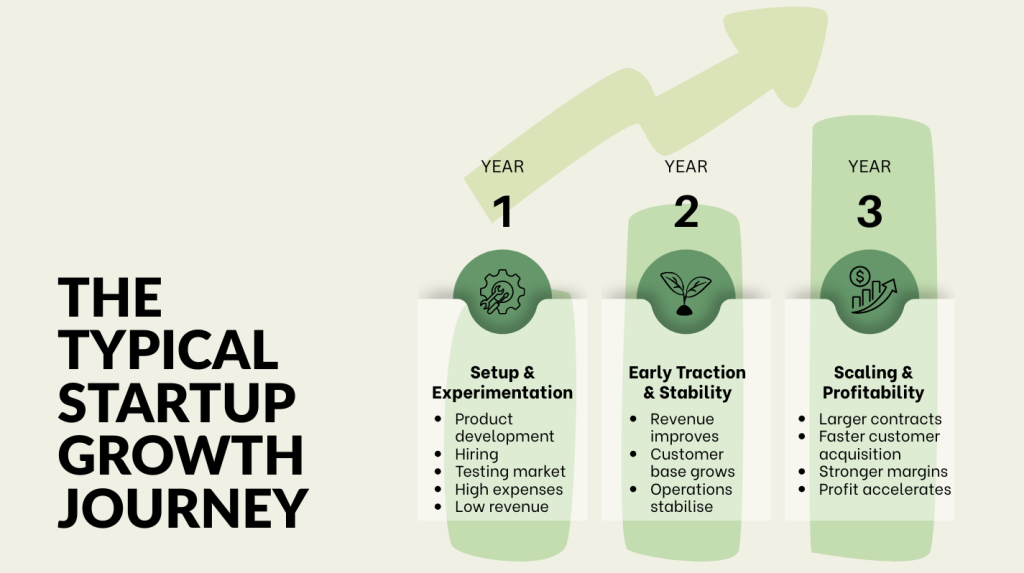

The goal is to ensure your highest-growth years actually land inside that 3-year window. To see why this matters, we can think about the typical startup journey:

Most startups do not become profitable immediately. The early stage is usually filled with experimentation, product development, and finding product–market fit. Revenue is often unpredictable, while expenses remain high.

If your SUTE window begins too early, part of the exemption may be used during a phase where there is little chargeable income to protect. This means that a portion of the benefit may be absorbed during the lowest-value stage of the business.

The real opportunity is to align the exemption window with the years where the company begins gaining traction and generating stronger profits. When structured well, more of your growth-stage earnings can fall within the SUTE period. That translates into stronger cash flow, which could help to extend the company’s runway long enough to reach the next stage of growth.

So if we assume a company incorporates in May 2026. The founder now faces a deceptively simple decision: “When should my financial year end be?” This choice determines when the first YA begins and when the three‑year SUTE countdown starts.

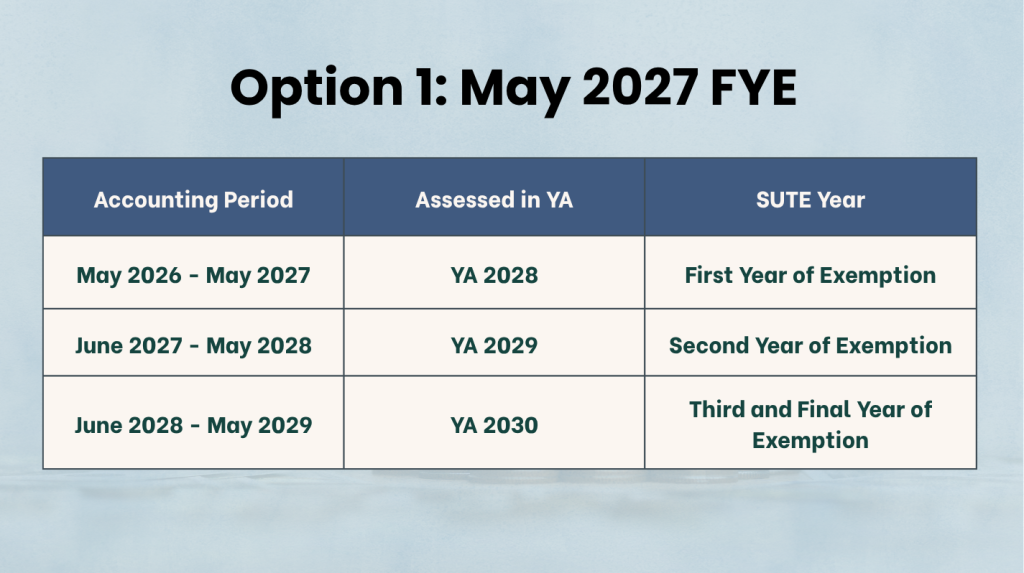

Option 1: Choosing May 2027 as FYE

You may choose May 2027 as your permanent FYE. By doing this, you give your company a full, uninterrupted 12-month runway for its very first accounting period. The first accounting period typically runs from the date of incorporation to the first FYE.

Your three SUTE exemption years will roll out like this:

By setting your calendar this way, you ensure that not a single day of your 3-year tax shelter is wasted on a shortened “partial year,” giving your business the maximum possible time to scale up its profits before the full tax rate hits.

As a result, you achieve three critical financial advantages exactly when your business needs them most:

1. More profits qualify: Aligning your exemption years with growth ensures that higher‑revenue periods fall inside the SUTE window.

2. Cash flow strengthens: Tax savings arrive when scaling costs are highest.

3. Capital stays in the business: More money remains available for reinvestment, extending runway and accelerating growth.

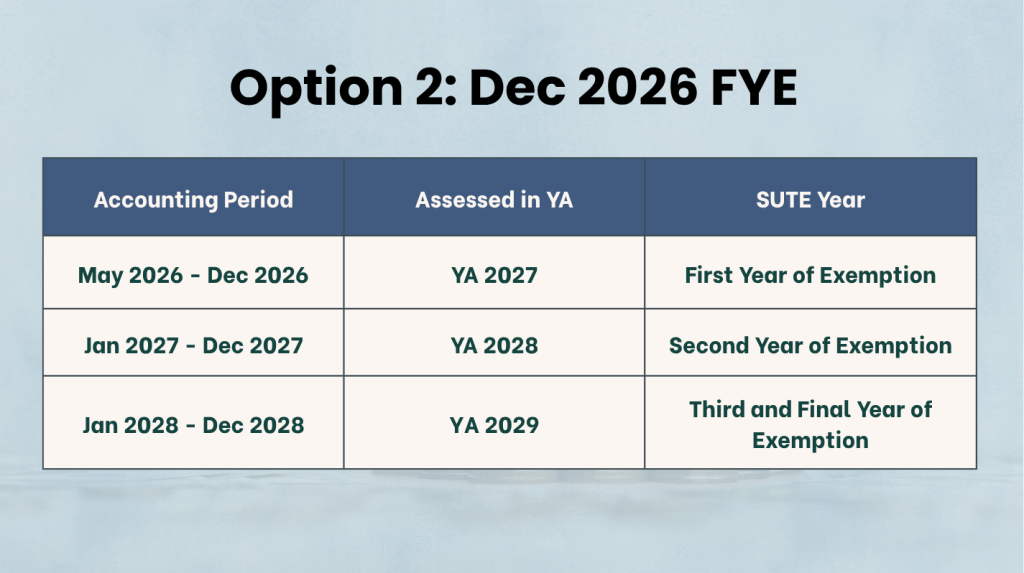

Option 2: Choosing Dec 2026 as FYE

Imagine you incorporate your business in May 2026 and select December 2026 as your FYE because it matches the normal calendar year. At first glance, this setup looks completely harmless. However, because of how Singapore’s tax clock works, your three SUTE exemption years will roll out like this:

Here’s the catch: YA 2027 covers less than 12 months of activity. On paper, you qualify for three YAs of exemption. In practice, this structure front-loads a partial year into your SUTE window, which means one of your exemption years is consumed during a period when the business may still be ramping up.

As a result, one full exemption year is used before the business truly gains momentum. In effect, your startup only benefits from about two years and seven months of meaningful tax relief, rather than the full three-year window.

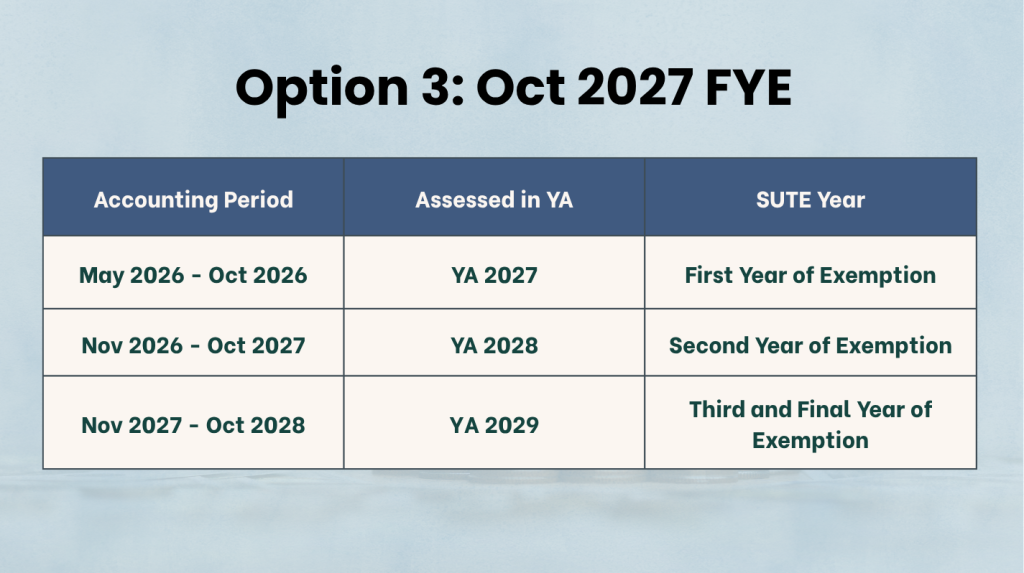

Option 3: Choosing Oct 2027 as FYE

Lastly, let’s look at what happens when a founder tries to “stretch” out the first financial year. Your company incorporates in May 2026 and decide to set its FYE as October 2027.

At first glance, this may seem like a smart way to “buy more time”. A longer first financial period seems like it would give the business more breathing room. However, when a financial period exceeds 12 months, it is typically split into separate basis periods for tax assessment purposes.

Here is how the SUTE timeline would effectively work in this scenario:

Although the company appears to have a single 18-month “first year,” the SUTE window is still consumed across 3 YAs. Importantly, YA 2027 is triggered during a period where the business may still be in setup mode, generating limited revenue or operating at a loss.

As such, one of the three SUTE years is used during an early-stage phase, when there may be little or no chargeable income to benefit from the exemption. This does not extend or enhance the SUTE benefit. Instead, it spreads the exemption window across a longer startup runway, which may or may not align with when the business becomes profitable.

The key takeaway is that extending your first financial year does not automatically improve tax efficiency. What matters more is how your financial year-end aligns with your business’s growth curve, so that your strongest profit years fall within the SUTE window.

Choosing the Best Path

Across all three options, one principle never changes: the SUTE benefit is locked to your first three YAs. The only lever you control is when those years begin relative to your growth curve. That’s why the best approach is the one that deliberately aligns your exemption window with the period when profits actually ramp up. The sweet spot is a structure that preserves all three years for your most profitable phase. This is achieved by incorporation timing and FYE so that SUTE shields your strongest early years.

The examples in this article are simplified for illustration purposes. Since every startup’s path is unique, professional guidance is invaluable. Speaking to an accountant can help you time your incorporation and FYE so it aligns with your growth curve. Founders should also refer to the official IRAS corporate tax exemption webpage for the latest guidance.

Conclusion: Timing Matters

Optimising your first three YAs under SUTE is about planning and timing. It comes down to the decisions founders make about when to incorporate, setting the FYE, and knowing when profits are likely to materialise. Once your first YA starts, the countdown begins. While you can always improve operations later, you cannot go back and redesign your early tax structure.

When you plan your first three YAs with growth in mind, you will have more cash to hire, build, and scale when it matters most. Conversely, if you miss the right timing, you are giving up cash you could have kept in the business. Structure things so the window lines up with your growth curve, not your pre‑revenue days. These are choices you get to make if you pay attention to them.

In Part 2, we will break down the most common pitfalls, and provide a practical checklist that founders should walk through before locking in their structure.

Stay ahead with exclusive insights! Sign up for our mailing list and never miss an article. Be the first to discover inspiring stories, valuable insights and expert tips – straight to your inbox!