What is Estimated Chargeable Income (ECI) Filing?

Most first-time founders in Singapore encounter Estimated Chargeable Income (ECI) only when a filing deadline is brought to their attention. At that point, they often have questions such as: “Do I need to file it?”, “Is this the same as my tax return?”, or “Why does Inland Revenue Authority of Singapore (IRAS) require an estimate of income?” This often leads to common misconceptions, like ECI is the same as corporate tax filing or that it is just another tax deadline.

Rather than waiting until every figure has been finalised, companies are required to provide an estimate of their taxable profits for a Year of Assessment (YA). This estimate is based on the best information available at the time. The word to focus on in ECI is “estimated.”The objective is to provide a reasonable picture of the company’s expected tax position based on the information currently available. ECI is basically asking: Looking at your current numbers, what do you reasonably expect your company’s taxable income to be for the year?

A common misconception is that ECI is the same as the company’s corporate tax return, but it is not. You can think of ECI as a forecast, while your corporate tax return is the final scorecard. ECI tells IRAS what you expect your taxable income to be shortly after your financial year ends. Your corporate tax return, which is filed later, confirms what the actual numbers turned out to be once your accounts and tax computations have been completed.

Why Do We Need ECI?

ECI is part of how Singapore runs a stable and predictable tax system. It serves 2 key purposes:

1. A Real-Time Signal for the Government

IRAS receives an early signal of how businesses are actually performing. Instead of waiting for final tax returns, the government gets a near real-time view of corporate profitability across industries. If certain sectors are growing faster than expected, or showing signs of slowdown, trends can be identified earlier and it allows the government to respond with targeted support measures.

2. A Cash Flow Mechanism That Works for Businesses Too

ECI also plays a practical role in how businesses manage tax payments. Once ECI is filed, IRAS may issue an early Notice of Assessment (NOA), which can unlock the option for instalment payments via GIRO. This unlocks the option to spread payments across several months instead of facing one large lump sum. This helps businesses manage cash flow more smoothly and preserve working capital for operations and growth.

Who Needs to File?

Most companies incorporated in Singapore are required to file ECI, unless they qualify for an exemption. If your company is actively operating or generating revenue, ECI is usually part of your annual compliance cycle. This includes:

- Singapore-incorporated companies

- Any company that has income or business activity in Singapore during the financial year

- Branches of foreign companies registered in Singapore

At the same time, IRAS recognises that not every company needs the same level of reporting complexity. That is why an administrative waiver exists for eligible companies, typically smaller businesses with low revenue and a NIL estimated tax position. This ensures that early-stage companies are not burdened with unnecessary compliance requirements.

The NIL ECI Filing Exemption

IRAS provides a filing exemption for companies that meet both of the following conditions:

- Annual revenue is S$5 million or less for the financial year

- ECI is NIL for the Year of Assessment (YA) (i.e. the company’s estimated taxable income is zero before applying any partial tax exemptions or startup tax exemption benefits)

For many early-stage startups in Singapore, especially in the first few years where the business is pre-profit or operating at breakeven after expenses, this exemption may be relevant. However, it is not automatic, and must be assessed and applied correctly.

A common misconception that founders have is that “If my company is dormant, I don’t need to file for a tax return.” If your company is completely dormant (i.e., no revenue, no bank transactions, no business activity), this often means you meet the exemption conditions for ECI filing. You are only outside the filing requirement if IRAS has formally approved your company for a waiver. If your company has not been granted this waiver, IRAS still expects you to file and submit a NIL return.

If you aren’t 100% sure, it is always safer to file a NIL return than to wait for an estimated tax bill.

When and How to File?

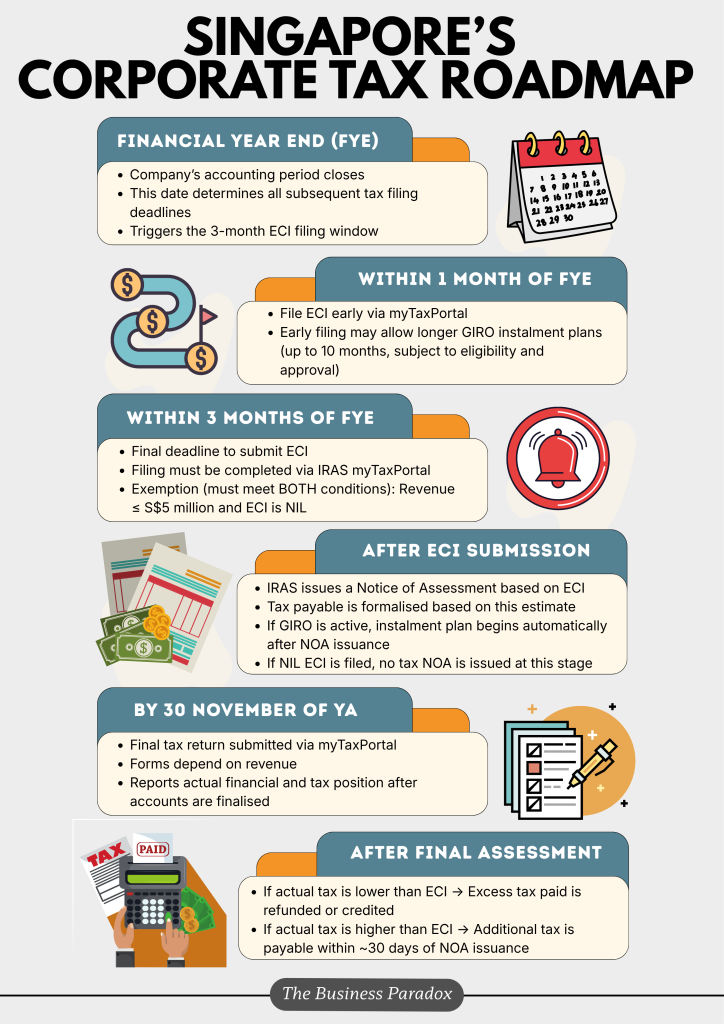

ECI filing follows one clear rule: it must be submitted within three months from the end of your financial year (FYE). For example, if your financial year ends on 31 December 2025, your ECI filing deadline is 31 March 2026. This deadline is fixed and strictly enforced. Since there is no buffer or grace period, finalising your management accounts early is essential to remaining compliant.

If ECI is not filed by the deadline, IRAS does not assume the company made a loss or qualifies for exemption. Instead, it may proceed to issue a NOA based on estimated figures using available information from prior filings or industry benchmarks. It is also important not to confuse ECI with your annual corporate tax return, they are separate filings with separate deadlines:

- ECI: Due within 3 months after FYE

- Corporate Tax Return: Due by 30 November of the YA

ECI is submitted online through the IRAS myTaxPortal, using your company’s Corppass account. The process is relatively straightforward:

- Log in to myTaxPortal using Corppass

- Navigate to the Corporate Tax → ECI filing section

- Enter your ECI for the relevant YA

- Submit the form electronically

- Once submitted, IRAS typically issues a NOA within a few days

What Happens After You File?

Once ECI is submitted, IRAS processes the information and issues a NOA based on the estimated chargeable income provided. This NOA sets out the amount of tax payable and the payment timeline. If a NIL ECI is filed, no immediate NOA is issued at this stage. In most cases, companies will either 1) pay the tax in a lump sum, or 2) opt for monthly GIRO instalments, if GIRO is set up and the company qualifies for an instalment arrangement.

After the financial statements are finalised, the company must file its Corporate Income Tax Return. This return is due by 30 November of the YA, regardless of the company’s FYE. At this stage, IRAS compares the final tax position against the earlier ECI filing. As such, maintaining clear working papers e.g., computation breakdowns allows founders or finance teams to explain any variances confidently.

ECI isn’t a one‑off task but a cycle of estimating, confirming, reconciling. When managed well, it creates a steady flow from early financial visibility to final tax settlement, replacing last‑minute stress with structured clarity.

Why Does ECI Matter for Singapore-Based Businesses?

For founders who understand how it works, ECI delivers distinct benefits: compliance, cash flow, and credibility. Importantly, each of these ties directly to the themes we’ve already covered, from Start-Up Tax Exemption (SUTE) to tax residency to the role of the corporate secretary.

1. Compliance

Filing your ECI on time builds a clean track record with IRAS. This makes a difference when your company applies for corporate bank loans, seeks regulatory licenses, or undergoes rigorous due diligence. Conversely, missing the deadline may signal to IRAS that your internal governance might be slipping. Repeated lapses can trigger penalties, audits, and closer scrutiny of tax positions. This connects back to the role of the corporate secretary in maintaining a governance paper trail. ECI filing is one of the most visible points in that trail.

2. Cash Flow

This is the most overlooked perk of the ECI. If you file within the three-month window and have an active GIRO arrangement, IRAS lets you split your estimated tax bill into monthly installments instead. The earlier you file, the more installments you get (up to 10 months). It is important to note that your GIRO arrangement needs to be set up at least three weeks before you file. For early‑stage companies, especially during the SUTE years, filing ECI early turns compliance into a cash‑flow advantage.

3. Credibility

A company that files accurately and on time, with chargeable income aligned to its SUTE structure and tax residency position, demonstrates that its compliance system works. It also connects directly to earlier steps: the SUTE exemptions flow through the NOA issued after ECI filing, and the governance record maintained by the corporate secretary supports the tax residency position that underpins SUTE eligibility.

One important point for founders to understand is that ECI is filed based on the company’s estimated chargeable income before applying tax exemptions and reliefs, such as the SUTE or Partial Tax Exemption. The figure submitted in the ECI filing represents the company’s estimated chargeable income. IRAS will then apply the relevant tax exemptions, rebates, or reliefs when computing the final tax payable and issuing the NOA. In other words, ECI is not about calculating your final tax bill. It is about providing IRAS with a reasonable estimate of your company’s taxable position, allowing the correct tax treatment to be applied when your assessment is issued.

Filing your ECI does not require highly specialised tax expertise. For most Singapore companies, an internal accountant, an outsourced bookkeeper, or your corporate service provider can handle it efficiently. The challenge lies not in complexity, but in coordination.

- Accountant’s Role: Holds the financial data and prepares the ECI estimate.

- Corporate Secretary’s Role: Monitors the compliance calendar and tracks the statutory deadlines.

The most common failure happens when these two functions are outsourced to different vendors who do not communicate. Each assumes the other is responsible, and ECI may fall through the gap. A few clear actions taken before year‑end can eliminate the risk of miscommunication.

Before the financial year end, confirm with both providers:

- When the filing will be done

- Who calculates the ECI figure

- Who files it with IRAS

Set the one‑month early filing target as the working deadline, not the three‑month maximum. This buffer ensures delays in preparing accounts don’t push filing to the last moment.

Activate GIRO early on. You cannot arrange an installment plan after IRAS issues your NOA. Hence, your corporate GIRO mandate must be active with IRAS at least three weeks before ECI is filed.

Conclusion: Build Your Filing Rhythm

ECI filing should not be a last-minute scramble. It is an estimate submitted within three months of your FYE, with clear exemptions available for eligible companies and potential cash flow benefits for businesses that plan ahead.

For founders, ECI is also where many earlier business decisions begin to come together. The foundations you establish from the start, such as appointing a reliable Corporate Secretary, understanding your Tax Residency position, assessing your eligibility for the SUTE, maintaining proper governance records, and choosing the right FYE, can influence how smoothly your tax journey unfolds.

This is why ECI is one of the first checkpoints after your financial year closes where your business structure, financial performance, and tax planning decisions translate into real outcomes. When approached well, ECI becomes a tool that helps businesses manage cash flow more effectively. Take control of the process early: set internal deadlines, align responsibilities with your corporate service providers, and establish a filing rhythm that keeps your business ready for what comes next.

This article does not constitute tax advice and provides general guidance on ECI filing obligations for Singapore companies as of June 2026. Filing obligations depend on your company’s specific situation and IRAS guidelines can change. For more information, refer to IRAS guidance on ECI Filing.

Stay ahead with exclusive insights! Sign up for our mailing list and never miss an article. Be the first to discover inspiring stories, valuable insights and expert tips – straight to your inbox!