Selling More Doesn’t Always Mean Making More

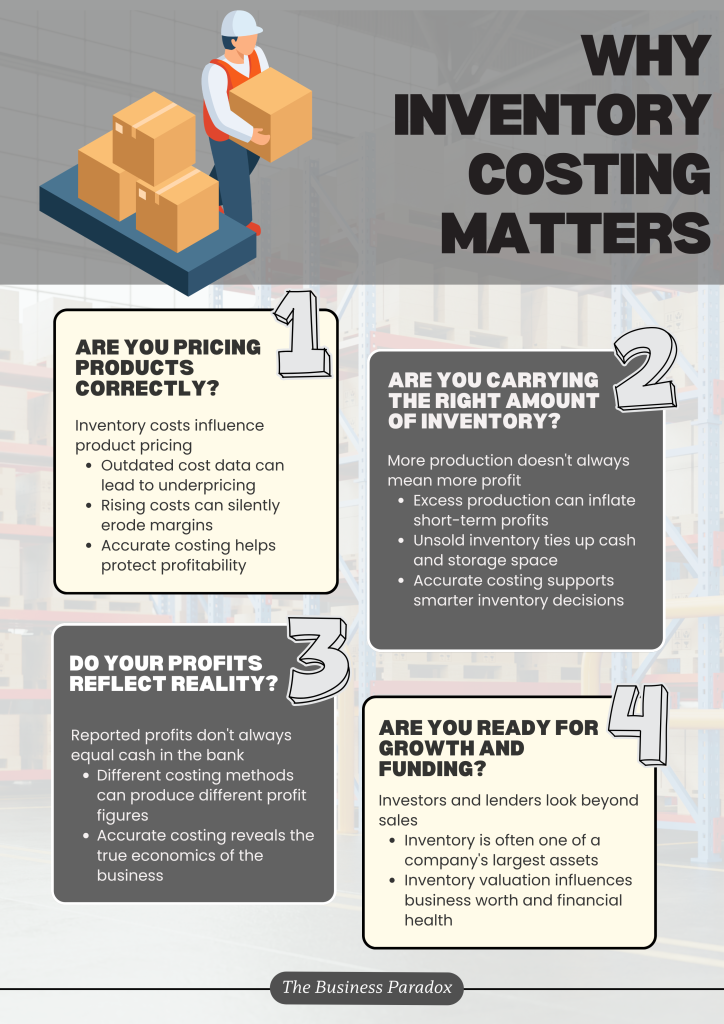

Sales were growing. Customers were buying your product. Orders were moving out the door. By most measures, the business was having a good quarter. Then the financial reports arrived and the profit was lower than expected. Had costs increased? Were margins shrinking? Was there a problem in the daily operations? After all, if more products were sold, shouldn’t profit follow? Not always. Behind every product sitting on a shelf, or waiting to be shipped is a number that most people rarely think about: what that inventory actually costs the business.

Before revenue, before expenses, before any number on your financial statements, there is inventory. The price you paid for it. When you paid it. How you account for it when it’s sold. Inventory costing often operates quietly in the background. Before a single sale is made, your profit is already being shaped by how your business values the inventory it holds. This seemingly small choice can shape some of the most important numbers used to guide the business.

You cannot have a reliable picture of your profitability without first having an accurate picture of your inventory. Your inventory costing method determines what counts as a cost when you sell a product. Change the method, and you change your reported profit, your tax bill, and your cash position without actually changing how your business operates.

This week’s article focuses on inventory costing and the hidden role it plays in shaping business performance. While it is often viewed as a technical accounting concept, inventory costing is also about understanding the economics of your business.

What is Inventory Costing?

Inventory costing is the process of determining how much a business’s inventory actually costs. This can include expenses such as shipping, storage, handling, and, for manufacturers, the costs of producing those goods. Every unit you buy, make, or store carries more than just its purchase price. Costs like production, storage, handling, and overhead all attach themselves to inventory. It answers a fundamental question: How much did it really cost to put this product in a customers hands?

The way you assign those costs directly shapes your cost of goods sold (COGS). Since COGS is subtracted from revenue, it affects profit, taxes, and the value of inventory reported on financial statements. Different methods can produce different financial results, particularly when prices are changing.

While inventory costing may sound complex, most businesses generally use one of three common methods to determine which inventory costs are assigned to products sold and which remain on the balance sheet as inventory.

1. First-In, First-Out (FIFO)

FIFO assumes that the oldest inventory purchased is sold first.

Imagine a retailer buys 100 units of a product at $20 each in January and another 100 units at $30 each in June. Under FIFO, when a sale is made, the system assumes the January inventory is sold first. As a result, older and typically lower costs are recorded as the COGS.

During periods of rising prices, FIFO often produces higher reported profits because lower historical costs are matched against current sales revenue. It also results in inventory values that are closer to current market prices since the newest inventory remains on the balance sheet.

2. Last-In, First-Out (LIFO)

LIFO assumes that the most recently purchased inventory is sold first.

Using the same example above, when a sale occurs, the system assumes the newer $30 inventory is sold before the older $20 inventory. This means higher, more recent costs are recorded as COGS. During periods of rising prices, LIFO typically results in lower reported profits because current revenues are matched against higher current costs.

However, lower profits can also mean lower taxable income, helping businesses preserve cash flow. While LIFO is permitted under U.S. accounting rules (U.S. GAAP), it is prohibited under International Financial Reporting Standards (IFRS) because it leaves outdated asset values on the balance sheet.

3. Weighted Average Cost

The weighted average method takes all inventory costs and calculates a single average cost per unit.

Using the same example, inventory purchased at $20 and $30 would be averaged to determine one cost figure. Every unit sold would then use that average cost, regardless of when it was purchased. This approach smooths out fluctuations in inventory costs and is often simpler to administer. Financial results typically fall somewhere between FIFO and LIFO.

Inventory valuation affects both the income statement and the balance sheet. FIFO typically results in higher inventory values and stronger reported earnings during inflation, while LIFO tends to show lower inventory values and more conservative profits. These differences flow through to key financial ratios used by investors, lenders, and analysts, shaping perceptions of financial health, efficiency, and stability.

The right choice for your business depends on factors such as industry practices, reporting requirements, tax considerations, and management objectives. What matters most is consistency and ensuring the chosen method provides an accurate view of profitability, inventory value, and business performance. The method you choose influences how profits are measured, how inventory is valued, and how confidently leaders can make pricing, purchasing, and growth decisions.

In essence, inventory costing is the framework that dictates which costs are recognised today and which are deferred for tomorrow.

The Price of Getting It Wrong

To understand how inventory costing can quietly make or break a business, it helps to look at what happens in the real world when this mechanism is mismanaged. Here are some common scenarios that show what happens when the numbers on your balance sheet lose touch with economic reality:

Example 1: The Retailer with “Profitable” Sales but Shrinking Margins

A retail boutique selling premium skincare products purchased its initial inventory at $20 per unit six months ago. Today, due to supplier price increases and higher freight costs, the same product costs $30 to replace. Yet the business continues pricing based on its original cost assumptions. Sales remain strong and profit margins appear healthy on reports. However, when it came to restocking, management discovers that a much larger share of their cash is needed to replenish inventory. The business was measuring yesterday’s costs while operating in today’s market. Since their costing method ignored real‑time price changes, they ended up underpricing products and draining their own cash flow.

Takeaway Lesson: If inventory costs are not regularly updated, businesses risk underpricing products and sacrificing profitability without realising it.

Example 2: The Business Paying More Tax Than Expected

A wholesale distributor operates during a period of rising costs and uses the FIFO inventory costing method. Because older, lower-cost inventory is matched against current sales, the company reports higher profits than it would under other costing approaches. At first glance, business looks more profitable and performance seems strong. However, when tax season arrives, the higher reported earnings translate into a larger tax bill. Cash that could have been used for expansion, hiring, or new equipment is instead paid out in taxes. The business appears wealthier on paper than in reality.

Takeaway Lesson: Reported profits and available cash are not always the same thing. Inventory costing can have a direct impact on both.

Example 3: The Manufacturer with a Warehouse Full of Inventory

A manufacturing company is under pressure to meet quarterly profit targets. To improve financial results, production is increased even though customer demand has remained unchanged. In the short term, the strategy works. By artificially spiking production, the system spreads fixed costs thinly across a massive volume of items. However, the company has simply converted costs into inventory sitting on warehouse shelves. Months later, management faces a different challenge: excess stock, rising storage costs, and cash tied up in products that have yet to be sold. What appeared to be a profit improvement was really an inventory problem in the making.

Takeaway Lesson: Producing more inventory can improve results temporarily, but it does not create demand, cash flow, or long-term value.

Example 4: The “Bestselling” Product That Was Never Actually Profitable

A food manufacturer has a popular snack bar that consistently ranks among its top-selling products. Encouraged by strong sales volumes, leadership allocates more marketing budget, production capacity, and investment toward growing the product line. However, the company’s costing system only captures direct ingredients and labour. Important costs such as packaging, storage, freight, and production overhead are not properly allocated to the product. When the company finally conducts a full absorption costing audit, they discover the snack bar’s production and distribution costs are higher than its shelf price. Due to incomplete cost allocation, the company’s resources were poured into a product that was quietly draining cash reserves instead of generating profit.

Takeaway Lesson: A product that sells well is not necessarily a product that creates value. Accurate inventory costing helps leaders distinguish between revenue growth and profitable growth.

What Every Leader Should Know About Inventory Costs

When you first start a business, inventory feels straightforward. You buy small batches, you know exactly what they cost, and your focus is on selling and refining your product. As the business expands, things start to shift. Raw material prices fluctuate, inventory builds up, production scales, and different batches of inventory may carry very different costs. Suddenly, the same ingredient or component that cost $10 a few months ago now costs $15. Your storeroom becomes a mix of identical items bought at very different prices. This is precisely when inventory costing becomes a leadership issue.

It determines how much of a product’s cost is recognised when a sale is made, how much remains on the balance sheet as inventory, and how profit is measured. If costs are rising but the business relies on outdated cost information, it may underprice products and unknowingly erode margins.

Inventory costing helps leaders separate operational reality from accounting appearance. A business may report healthy profits while excess inventory quietly accumulates in the warehouse. Conversely, a company may appear less profitable on paper while actually generating strong cash flow and creating long-term value. Understanding inventory costing helps leaders look beyond the headline numbers and make decisions based on what is actually happening in the business.

Inventory costing has a ripple effect across many parts of a business. It directly shapes gross profit by determining how costs are matched to revenue, meaning that in rising price environments, methods like FIFO can inflate margins on paper and create a false sense of profitability. It also influences cash flow, since inventory purchases consume real cash long before they appear on the income statement, and poor costing visibility can lead to excess stock that ties up working capital. Tax outcomes are also affected, since different costing methods produce different cost of goods sold figures and different taxable profits, making transparency essential.

When done well, it provides leaders with a clear view of product profitability and operational performance. But when it is done poorly, it replaces reality with approximation, leaving decisions to be made on numbers that only partially reflect what is actually happening. The better leaders understand the true cost of the products they buy, make, and sell, the better equipped they are to price and allocate resources effectively.

Conclusion: From Products to Profits

Ultimately, choosing an inventory costing method is a strategic decision that shapes your corporate narrative and preserves your cash flow. Inventory costing is often treated as a technical accounting detail, but it sits much closer to the heart of business decision-making.

As seen through the different costing methods and examples, the same business can report very different levels of profitability depending on how inventory costs are assigned. From the retail boutique that unknowingly underprices its products, to the manufacturer that overproduces to hit earnings targets, the consequences of poor costing ripple across cash flow, investor confidence, and long‑term sustainability.

Inventory costing doesn’t just measure performance, it has the potential to actively shape it. When managed well, it grounds decisions in reality and guides smarter pricing and resource allocation. Conversely, when managed poorly, it clouds true profitability and gradually erodes competitive strength. In the end, companies also compete in how clearly they understand their own costs.

Stay ahead with exclusive insights! Sign up for our mailing list and never miss an article. Be the first to discover inspiring stories, valuable insights and expert tips – straight to your inbox!