Many have touted the arrival of blockchain technology as the next frontier in business operations, a pioneering breakthrough that possesses the potential to transform conventional procedures across industries. Often associated primarily with cryptocurrencies like Bitcoin, the application of blockchain goes far beyond this investment phenomenon. To understand blockchain technology’s potential impact, we must first examine the fundamentals of this groundbreaking approach.

At its core, blockchain is a decentralized system where all transactions or digital events get consolidated into ‘blocks’ and distributed across a network of computers, referred to as ‘nodes’. Each block contains a cryptographic hash of the previous block, a timestamp, and transaction data. The unique attribute of this system is its ability for self-audit – a quality that ascertains data integrity and provides unparalleled transparency.

“A blockchain is, in the simplest of terms, a time-stamped series of immutable records of data that is managed by a cluster of computers not owned by any single entity. Each of these blocks of data is secured and bound to each other using cryptographic principles.”

With the foundational definition established, it’s essential to watch the emergence of an innovative application of this technology – ‘blockchain accounting‘. This development breaks down traditional accounting paradigms and propels the industry towards a more efficient, transparent, and secure future.

Understanding the Basics of Blockchain Accounting

The transformative influence of blockchain technology is becoming conspicuously apparent in the accounting sector. Positioned as a cutting-edge technology of trust, blockchain stands as an innovation, assuring security, transparency, and immutability of financial transactions. It fundamentally embodies an unalterable public record of data managed by a cluster of computers, not confined by a single entity.

Blockchain accounting refers to the practice of leveraging blockchain technology to record, validate, or audit transactions. Offering a cryptographically securitized record with zero downtime and shared access, blockchain accounting stands to tackle many current accounting challenges such as errors, fraud, and inefficiency.

- Record: Blockchain allows for automatic recording of every transaction, down to the smallest detail, onto its decentralized ledger, providing a complete historical record for each asset.

- Validate: Transactions on the blockchain are validated by a consensus of nodes in the network, thus, ensuring accuracy, consistency, and integrity.

- Audit: This technology’s immutable nature makes it a perfect tool for audits, eliminating data manipulation and providing auditors with indisputable audit trails.

Resultantly, blockchain’s inherent properties are fostering a robust infrastructure for accounting. The deployment of these distributed ledgers ensures complete traceability of transactions, thereby mitigating the risk of financial malfeasance while elevating the efficiency of reconciliation procedures. The verifiable and immutable nature of blockchain transactions offer a clear audit trail, disrupting traditional accounting methods.

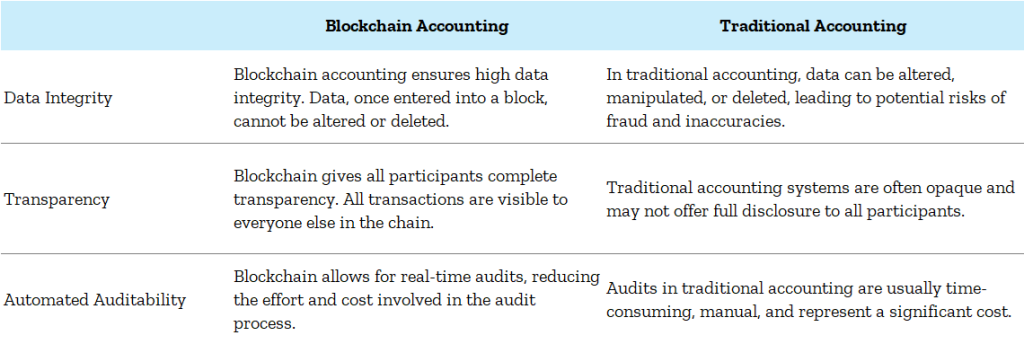

Blockchain Accounting vs. Traditional Accounting

As the metamorphosis from traditional accounting methods to blockchain accounting takes its course, it becomes necessary to reveal the stark differences and similarities that exist between these two paradigms.

Unlike traditional accounting which heavily relies on intermediaries such as auditors, blockchain accounting is a decentralized system, eliminating the need for a third-party authority. This method democratizes transaction processing and allows for a high degree of transparency in the financial realm. The transparency intrinsic to blockchain offers stakeholders an unparalleled level of trust in accounting records. On the one hand, this transparency is laudable; on the other, it might raise issues around financial privacy which traditional methods have been designed to maintain.

Furthermore, while traditional accounting operates on a closed-system that allows adjustments and modifications to transaction records, blockchain accounting is predicated on the fundamental principle of immutability. This means that once a transaction is posted on the blockchain, it cannot be altered or deleted, subsequently ensuring a permanent and tamper-proof record. This attribute significantly mitigates fraud risks and human errors, which are inherent in the conventional system.

However, it’s worth emphasizing the intersection where traditional accounting and blockchain accounting methodologies converge. They both ultimately serve in maintaining financial integrity and promoting economic stability. Despite the existing differences, these two accounting methods continue to coexist and serve dual-purpose, providing the foundational architecture for a new kind of auditing system that amalgamates the best of both worlds.

In essence, adoption of blockchain accounting would require organizations to grapple with foreign concepts and novel protocols. Yet, with its distinctive ability to capitalize on its inherent advantages—transparency, security, efficiency and reduced costs—blockchain’s transformative potential in the domain of accounting cannot be underestimated.

Mechanics of Blockchain Accounting: How Does It Work?

Blockchain accounting works by managing three key components: digital assets, a blockchain record-keeping system, and smart contracts. Each aspect provides a unique function, enhancing the overall effectiveness of the system.

Digital Asset

Blockchain accounting uses digital ledgers to manage transactions. These ledgers are decentralized and updated using advanced cryptographic methods and sometimes, consensus algorithms. This guarantees that each transaction is unique, transparent, and secure. Transactions are logged, validated through various decentralized systems, and then added to the existing transaction chain.

This results in a series of records that are constantly updated, comprehensive, and irreversible. Blockchain’s method also avoids the scalability issues common in traditional accounting systems as increasing transactions only require more computing power.

The Blockchain Record-Keeping System

With all transactions being publicly visible, blockchain accounting is noted for its transparency. Modified or deleted transactions are impossible once they are approved, lowering the risk of financial fraud. Should fraud occur, it’s easily traceable and detectable, improving accountability. This also adds an unprecedented level of trust and security to financial record-keeping.

Smart Contracts

The use of smart contracts in governing transactions adds to blockchain accounting’s effectiveness. These contracts are self-executing, with their terms coded directly into them. Smart contracts eliminate intermediaries and ensure contract conditions are strictly met. This reduces administrative time and decreases discrepancy occurrences, leading to more efficient financial processes.

An example of blockchain accounting in practice is in a supply chain transaction. Once a product is delivered, a smart contract verifies the terms, initiating payment. The transaction is then recorded, verified, and approved on the blockchain ledger, leaving a permanent, transparent record. This exhibits the efficiency, security, and automation that make blockchain accounting unique.

Implementation

Combined, these elements of blockchain accounting provide a more efficient, secure, and transparent framework. However, widespread adoption of this system presents challenges, primarily due to regulatory issues and technological understanding.

Blockchain accounting has substantial potential benefits but also poses risks due to the absence of standardized regulations. International regulatory bodies are required to establish uniform rules for adopting blockchain.

Furthermore, the nuances of this evolving technology are not fully understood within the accounting industry. To enable smooth adoption, it’s crucial to close this knowledge gap and promote blockchain as a valuable tool.

Incorporating Blockchain Accounting into Your Business: A Step-By-Step Guide

Undoubtedly, the integration of blockchain accounting into your business operations can be a transformative strategy, given the myriad of benefits it offers from increased transparency to enhanced security. Yet, it’s crucial to understand the specific steps required to ensure a smooth transition to this avant-garde technology.

Journeying towards the mainstream adoption of blockchain accounting may present challenges, but the associated merits signal an optimistic future for those willing to step into this digital frontier. In a business landscape that is increasingly digital and complex, staying at the forefront of technology, such as embracing blockchain accounting, can offer an edge that leads to formidable strategic advantage.

Phase 1: Assess

The initial phase involves a meticulous evaluation of your current accounting systems. This scrutiny centers on the identification of areas where blockchain’s characteristics can deliver maximum value. It is a process that demands rigorous operational auditing, coupled with a profound understanding of how blockchain technology can revolutionize your accounting procedures.

Phase 2: Strategy

Once you have identified potential applications, the next step is to strategize the integration of blockchain technology. Devising a well-thought-out strategy is paramount in avoiding pitfalls during the implementation process. It’s recommended to engage with experienced blockchain developers and accounting experts who can guide you in constructing a blueprint for application. This blueprint should address the technical aspects of blockchain, its integration into existing systems, and the necessary training for your staff to competently navigate this new interface.

Phase 3: Implementation

Following the strategizing phase, the technical implementation of the blockchain platform takes precedence. Selecting the appropriate blockchain type, private or public, based on your organization’s needs and desired level of transparency, is a significant part of this phase. Furthermore, the development of smart contracts – self-executing contracts where the terms are directly written into code – must be handled adeptly. These contracts play a vital role in facilitating, verifying, and enforcing the negotiation of a transaction, ensuring a seamlessly automated accounting process.

Phase 4: Testing

Since the integration of any novel technology poses inherent risks, a stage of intensive system testing trails the technical implementation. This step serves to identify any flaws in the system and rectify them timely, minimizing the probability of system disruptions upon deployment. It is an essential step that provides assurance of the system’s robustness and reliability before it is brought online.

Phase 5: Evaluation

Finally, once the reliability of the system has been established and assurances of its security have been obtained, the transition to the live environment begins. Even after going live, it is critical to arrange for regular system audits and updates to ensure optimal operation and to maintain the integrity of the blockchain accounting system.

The Promising Future of Accounting with Blockchain Technology

The aftermath of blockchain implementation into the domain of accounting is worth evaluating. Contemplating the capabilities of blockchain technology, discussed priorly, it is conceivable that its adoption in accounting can foster efficient, transparent, and secure accounting processes. This outcome represents a paradigm shift from the more traditional processes that have been laden with complexity and opacity.

Blockchain’s decentralised and immutable nature allows for real-time auditing, potentially leading to improved regulatory compliance and overall transparency. Gone will be the days of intense scrutiny and laborious auditing exercises, as the tool would be equipped with contemporaneous oversight capabilities. Verifying the validity of transactions will no longer hinge on the circulation of paper-based documents or manual input, thus reducing the likelihood of human errors, and fundamentally streamlining the accounting process.

According to Mary Barth, a scholar at the Graduate School of Business at Stanford University, “Blockchain’s distributed ledger could provide an automatic audit trail of all transactions, increasing the efficiency of audits and reducing the costs of compliance.”

However, as we delve deeper into the perennial opportunities that blockchain holds, it is crucial to bear in mind the challenges that lie ahead. Blockchain’s impact on job skills and roles in the accounting profession is configured to be profound, necessitating a significant revamp in mindsets, skills, and tools to reap benefits derivable from this technology. Adapting to this disruptive force might entail investing in employee adaptation and upskilling programs, but the dividends are likely to be substantial in terms of operational efficiency and cost-effectiveness.

Additionally, the ability to achieve consensus among various stakeholders concerning the standardization of blockchain technologies and interoperability protocols will be critical for maximizing the potential of blockchain in the accounting sector.

In conclusion, while embracing blockchain technology does demand considerable industry augmentation, the trajectory towards such an evolution appears to be almost inevitable. With appropriate transformation management, blockchain accounting could indeed redefine our understanding of efficiency and transparency in the accounting industry.

Wrap-Up

In the digital age, technology continues to accelerate the pace of change and interaction among businesses. With blockchain accounting cementing itself as a impressive disruptor, businesses and accounting professionals need to harness its potential to maintain a competitive edge and to promote transparency in their financial operations.

For firms contemplating a shift to blockchain accounting, understanding the mechanics of how it works is crucial. Thanks to the straightforward yet firm transaction verification and recording protocols, blockchain technology ensures stringent bookkeeping while allowing for real time audits. Through its transformation of the traditional accountancy role, blockchain accounting is set to revolutionize age-old financial procedures and offer cost-saving benefits to companies.

Furthermore, the future of blockchain accounting promises to be disruptive, creating transformative effects that will likely resonate across the entire field of accountancy. Accountants are poised to embrace this technology as it evolves, becoming strategic advisors who provide value-added services rather than focusing on data entry and transaction verification.

Ultimately, the promising trajectory of blockchain technology in revolutionizing the accounting domain cannot be understated. It is predicted to be an enduring game-changer, moving the world towards a more secure, efficient and transparent financial ecosystem. As we continue to acquire a more unabridged understanding of this technology, its widespread applicability and benefits will undoubtedly reshape the future course of the accounting industry.